A Black-Scholes widget

A Black-Scholes widget

A Black-Scholes Widget Ready to Import and Export data via its Sockets (Inlets & Outlets)

Either the Option Price (left) or the Volatility (right) should be selected as Input and the other will automatically be calculated.

icon. Additional parameters of the modeled option, including the important Option metrics known as the "Greeks", are displayed in these sections as calculated by the model. In the "Contract Values" the intrinsic and extrinsic values of the contract is shown.

icon. Additional parameters of the modeled option, including the important Option metrics known as the "Greeks", are displayed in these sections as calculated by the model. In the "Contract Values" the intrinsic and extrinsic values of the contract is shown.

Greeks and Contract Values in BS widget

Getting Real-Time Data from Option Widget

. If this icon is clicked, a graph widget is automatically opened, which is then connected to the *BS* and visualizes the corresponding calculated data.

. If this icon is clicked, a graph widget is automatically opened, which is then connected to the *BS* and visualizes the corresponding calculated data.

Displaying the Graph of the BS

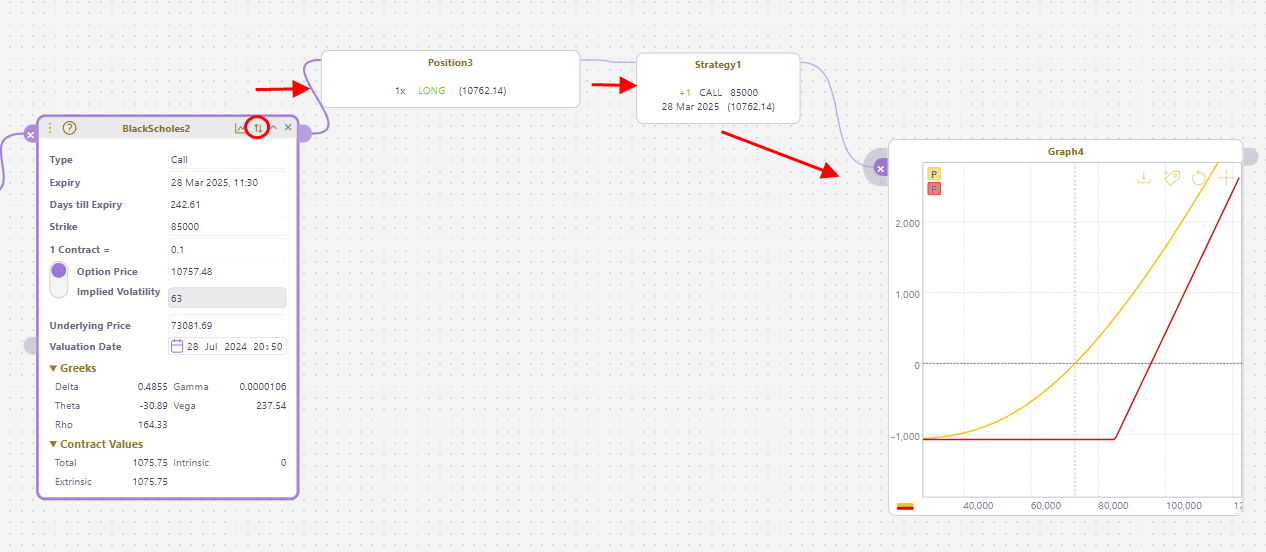

in the top right corner of the *Black-Scholes* widget opens a box. The user can enter the side and size of a position. Subsequently, a *Position* widget, a *Strategy* widget, and a *Graph* widget are automatically created, displaying the Black-Scholes data as a position.

in the top right corner of the *Black-Scholes* widget opens a box. The user can enter the side and size of a position. Subsequently, a *Position* widget, a *Strategy* widget, and a *Graph* widget are automatically created, displaying the Black-Scholes data as a position.

BS Can turn into Position using Position Icon

Turning a BS to a Positon by its included shortcut

Linkable Widgets Appear by Right-Click on BS Outlet